By: Pamela Martinez, JBS Corp

What is credit? How do I build my credit? A lot of us don’t find the right answers until substantial damage has been done. In the United States, you are defined by two numbers, your social security number, and your credit score. Your social security number is your ultimate identification, and your credit score determines your creditworthiness. It sounds harsh, but it’s the unapologetic truth. If you’ve ever considered applying for a credit card, moving out on your own, buying a new car, or taking out a student loan, it is important to understand how the credit score works.

Your credit score is a number assigned to you, ranging from 300-850, used by lenders, or “creditors” to determine whether you are a viable candidate to receive a loan. We all start out with no credit scores, and as we make credit-based decisions, which for most of us comes with financing our first car, applying for our first credit card, or acquiring student loans. Generally, assuming you are taking care of your credit from the start of your credit line, you land somewhere in the 600s. Going under 600 means you have multiple credit mistakes lingering on your report, and a score above 700 means that you have yet to make drastic mistakes.

Here is how the credit score range is broken down:

Your credit score is certainly not a fixed number; this number will fluctuate for all of your adult life.

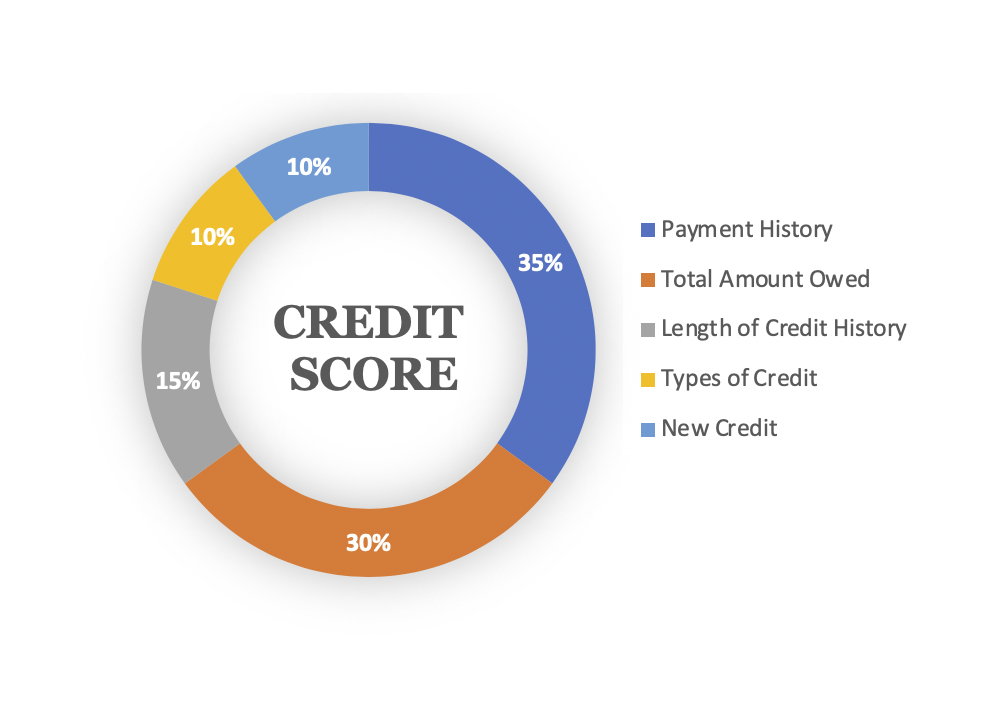

TransUnion, Equifax, and Experian are the three major credit reporting agencies, or credit bureaus, that report a person’s credit score. Below are the five factors used in calculating an individual’s credit score:

Payment History (35%)

Payment history is the most impactful component of your credit score. Submitting on-time payments on loans and debts you owe (even if it’s just the minimum payment) is paramount to ensure stability in your credit score. The smallest mistake carries a lot of weight, and late payments can last up to 7 years on your credit report!

Late payments have detrimental effects, regardless if you have a poor or excellent credit score, the penalty remains the same. You must do your best to never miss a payment. The easiest way to ensure this is to make it a habit to automate minimum payments on each credit account the moment you open it. I cannot imagine how organized humanity must have been before autopay…

Total Amount owed or Utilization (30%)

The total amount owed is your overall credit utilization rate, which is your total debt divided by your total available credit. Having a high utilization rate indicates that you use too much of your available credit and will negatively impact your credit score. Maintaining a low utilization rate, under 30%, lets creditors know that you are responsible.

For example, let’s say you have $10,000 available to borrow from your 4 credit cards. Assuming you owe $250 on each credit card, this is a total utilization of $1,000 out of your available $10,000, giving you a utilization rate of 10%.

Length of credit history (15%)

This is the average age of your credit lines- average age amongst all your credit lines. Keep all accounts open as long as humanly possible. This, of course, is tricky when you start off, as all your credit is brand new. The lesson here is to be careful when applying for new credit, realizing that each new line is like a newborn infant, aged 0, dramatically dragging your average age of credit history. Another issue arises here when you pay an account down to $0. Unfortunately, that car loan that you may be finishing up is adding 4 years and 6 months to your average credit age. I bet you never thought it would be a negative thing to pay off a debt…

The good news here is that mortgages, student loans, and old credit cards go a long way in increasing your average age as time goes on.

Types of Credit (10%)

The two types of credit used are known as revolving credit and installment credit. Revolving credit is credit lines and credit cards. In other words, you have access to borrowed money but don’t have to use it, and it is paid back with interest as you borrow. Installment credit, on the other hand, is a specified loan amount paid over a fixed time with monthly payments. Some examples include mortgages, car loans, student loans, personal loans, etc.

This one is simple, as most of us will have a well-diversified credit report just from normal financial activities such as buying a car, going to college, and buying a house.

New Credit (10%)

New credit refers to when a company or organization runs your credit report (pulls your loan). To make sure this part of your credit score is strong, try to limit the number of credit applications and be sure you are not applying to too many credit lines. Each one takes its toll.

Side Note: When applying for a student loan, personal loan, or car loan, you can “shop around” while only receiving one negative “credit pull.” Be sure you are getting the best deal in town!

- You must use your credit card for your score to go up – this is perhaps the most significant myth when it comes to credit. Some things you should know:

- 65% Of your credit score depends on debt repayment and debt utilization – so if you are paying on time and not borrowing too much, you are in good standing

- If you owe $0 on a credit card, it ACTUALLY COUNTS as an on-time payment!

- Not owing anything on your credit cards makes the credit use (or utilization) an automatic 0%, increasing the portion of your credit score that is determined based on utilization.

- The downside: The only negative that can come from not using your credit card is that the creditor may decide to close your account for inactivity. To avoid this, simply use each credit card for a specific purpose (gas, Netflix, coffee, etc.) and make sure you have autopay on!

- Checking your credit report will hurt your credit score,

- Companies like CreditKarma enable you to view your credit score without impacting and suggest best practices on improving your score – for free. The government also sponsors one free credit report per year from EACH credit bureaus, totaling 3 free credit reports per year. These can be found at annualcreditreport.com and do not harm you whatsoever.

- Once your credit score is poor, it’s impossible to rebuild it.

- Your credit score is subject to change, and many proactive measures can be taken to raise it. Having a bad credit score means that the rebuilding process will take longer, but it’s not impossible.

Please leave all questions, comments, or concerns in the comments below, and we will be sure to share some standard Credit Hacks specific to your situation.

WARNING! As you begin the journey of rebuilding your credit score, beware of “credit coaches” and “credit gurus.”. Credit repair is a $3 billion industry that exploits consumers for an average of $130 a month, offering services that someone can complete independently.

If this article is of interest to you, please let us know, as we at JBS are considering creating a “repair your credit” course if enough interest exists.