By: Rob Aquino & Pamela Martinez, JBS Corp.

The Paycheck Protection Program (PPP) Loan was one of the primary sources of relief offered by the U.S. Small Business Administration during the COVID-19 pandemic. The PPP loan gave small businesses short-term loans of 2.5 times their average monthly payroll expenses at a 1% interest rate. It offered full forgiveness if the funds are utilized for qualified expenses. The PPP loan was designed to help businesses remain open and afford to continue paying their employees—while simultaneously minimizing the number of citizens collecting unemployment benefits. Although the PPP loan helped thousands of businesses, it has risks that you may not have considered for this coming 2020 tax season.

Disclaimer: This article is not explaining how the PPP works but merely describing potential risks.

Unmet Requirements

Many have been blinded by the benefits and promises of the PPP loan; however, it is important to remember it is still a loan, and forgiveness is not guaranteed. The SBA states that for your PPP loan to be forgiven, at least 60% of the funds must be used for payroll expenses, the remaining 40% (or less) must be used for utilities, rent/mortgage, or interest; AND businesses must be back to regular full-time employees (FTEE) by a specific date.

The FTEE requirement is tricky. It enables you to choose your lowest FTEE from three different periods (in your business’s history) and use this number as your target FTEE. But what happens if you don’t/can’t reach the FTEE requirement? Not all hope is lost. For example, if you get to 50% FTEE that equates to 50% of the funds being forgivable, the remaining balance will be treated as a loan.

If the requirements mentioned above are not met, it’s unlikely that the entire loan will be forgiven, and the liability will fall on you. Alternatively, let’s say you do meet these requirements—the loan isn’t automatically forgiven—there is a ten-month window from the last day of your covered period. If you fail to apply for forgiveness during this period, payment deferment will end, and the loan burden will fall on you. Keep in mind that this is a two-year loan, and if not handled correctly, you may be responsible for having to pay back large sums of money in a short period of time.

There are excellent resources on the web, such as this article by InsideCharity, that provide an in-depth explanation of how to make sure you qualify for forgiveness. It would be best if you also consider consulting with your tax, legal, or financial advisor.

Taxable Income

Assuming forgiveness is granted on any provided PPP funds—a grant is generally not taxable income. The expenses that the grant was utilized for (payroll benefits, rent, mortgage, utilities) may not be deductible to your business income this year. This means you may see significant changes reflected on your profit and loss statement and expect to receive a higher tax bill this coming 2020 tax season.

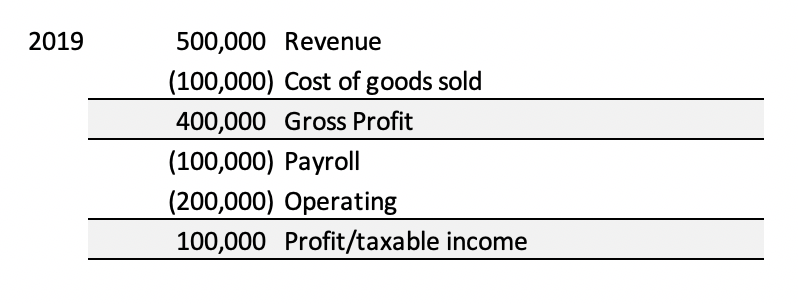

For example:

Here we see a hypothetical scenario in which a business made $500,000 in revenue for 2019 (pre-COVID) with a taxable income of $100,000.

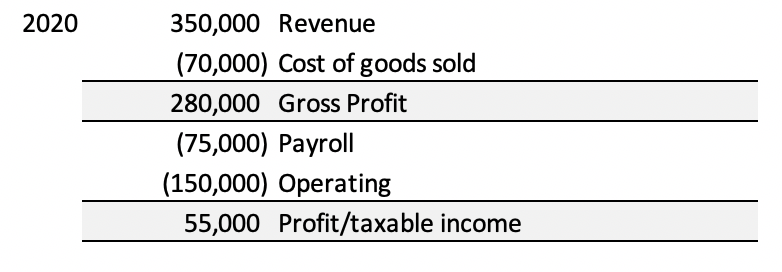

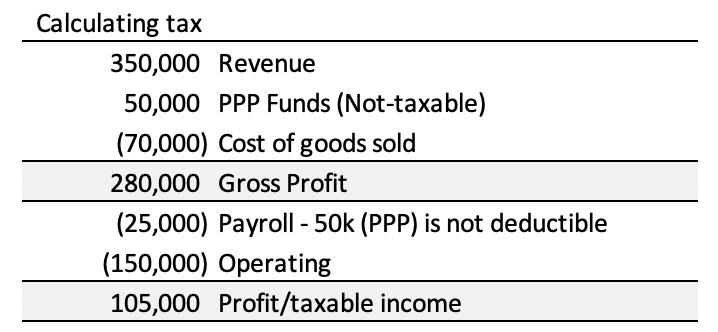

A business affected by the pandemic in 2020 has a projected revenue of $350,000 and a taxable income of $55,000. However, this business received $50,000 in PPP funds and qualified for full forgiveness. What does this mean?

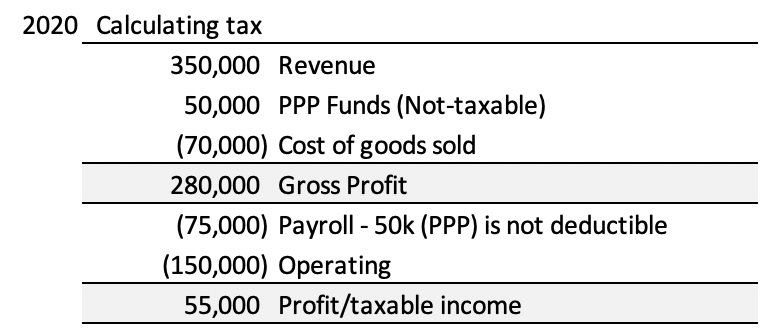

Under different circumstances (i.e., without the $50k PPP loan), the business would be expected to pay approximately $13,750 (estimate of tax at 25%) in taxes for 2020. However, after taking away the $50,000 PPP funds from their payroll costs, the businesses projected tax liability may look something like this:

Because the PPP loan covered the business’s payroll expenses and deducted from the business’ income, the PPP essentially becomes taxable income. Although the business only made a profit of $55,000 in 2020, their taxable income is now $105,000, and they are likely to pay a total of $26,250 (estimate of tax at 25%) in taxes—a total tax increase of $12,500 (nearly double!)

Now, we are all hoping that Congress realizes this and creates a special one-time rule to allow for the normal deductibility of the payroll expenses incurred but funded through the PPP. Regardless of whether Congress will adjust, these are merely assumptions. All businesses should behave as if this money will be taxable and should plan accordingly.

If you’d like more information or would like to begin planning for your corporation’s 2020 tax liability, please contact us at Pmartinez@jbscorp.net.