By: Pamela Martinez, JBS Corp.

Budgeting is like going to the gym. Almost everyone hates it—suffering through a series of trial and error working towards a viable solution—but we keep going and establish a routine that works best for our bodies ultimately, our goal is to improve. In any case, the first few attempts at sticking to a budget usually fail. The frameworks in place to create a budget are flawed; most are built on the conviction that money is spent consciously. However, money is a tool, a means to an end, and we generally don’t think twice before spending it on the things we want. So, if money is an unconscious tool, then why are we trying to budget consciously?

People often pursue strict and complicated budgets that don’t take into account the mishaps of everyday life, making it challenging to adhere to; In many cases, debt is the issue—if you relate to this, you should revert to our Snowball article.

Simplicity is key. The objective of a budget is to eliminate stress, achieve financial goals, and, by definition, should not be complicated. The budgeting strategy we are going to discuss is straightforward, simple, and, hopefully, the last one you create. First and foremost, when creating any budget, you should always begin with establishing your current financial standing. From there, you can move onto identifying your needs and your business goal. Your needs are the expenses you unequivocally cannot evade, i.e., taxes, housing, transportation, food, while your financial goals focus on saving for retirement or paying off debt.

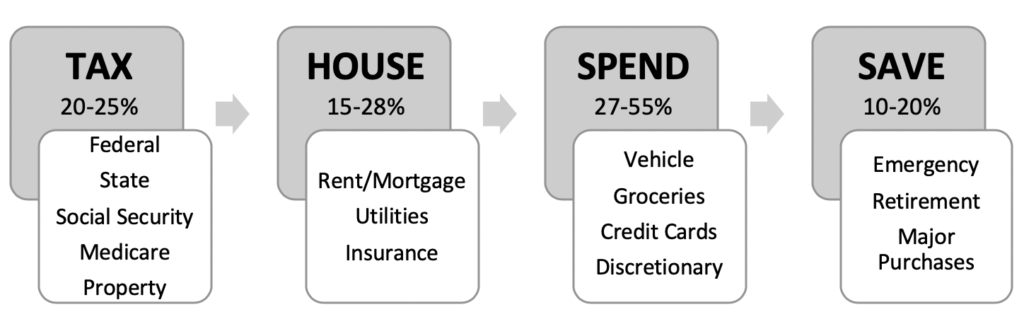

Think of your budget in four categories:

“Tax,” “House,” and “Spend” are your needs, and “Save” are your financial goals. Simple, right? Pay your needs and save your goals. There are the dollars you keep, and the dollars you give away.

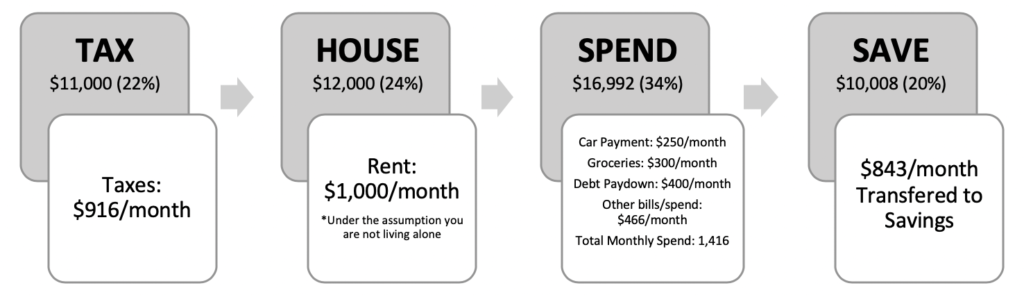

For example on an $50,000 gross annual income:

Remember, things may come up and you may need to spend more money, but in this scenario, you ARE saving $834 per month… if need be, you have money!

*Disclaimer: This is merely an example, and percentages and monthly costs should be adjusted to meet your financial standing.

Now, for a more rewarding approach, challenge yourself, and swap “Spend” and “Save.” Utilize “pay yourself first” philosophy, which affirms that an individual should save before they spend. Instead of buying yourself a brand-new Audi for $50,000, buy yourself, Honda, for $15,000 and apply the difference you’ll be saving on car payments towards your personal savings. By doing this, you’re ultimately paying your future self. Then perhaps you can truly afford something much nicer than an Audi and a Honda one day.

Saving money should not be a challenging task. To ease the anxiety provoked by saving, instead of telling yourself you’re going to stop eating out and quitting cold turkey, start small, and try telling yourself you want to save $500. Once you change your mentality, osmosis will take care of the rest, and you’ll find yourself saving more than you spend in no time. Try automating your savings, using tools like a 401(k) that withdraws money directly from your paycheck or having a fixed percentage of your pay be directly deposited into a savings account.

Equally important is the employment of self-discipline, regardless of how meticulous a budget might be; it won’t survive on its own. Money is systemically viewed as a powerful instrument of the intellectual, meaning that to obtain true wealth, one must be professionally successful and well versed in financial knowledge. When, in fact, the path to wealth is not built on expertise and income but rather on a robust, realistic budget and ethical money philosophies. Financial success requires good habits, not specialized knowledge.